Financial Crime: 3 Essential Tips To Prevent It

Financial crime is one of the biggest issues on a global level for many years now. It all looks like a cat-and-mouse game without the chance for any of the sides to win completely.

However, while financial crime is here to stay, that’s no reason why you should let it slide in your company. There are certain methods you can implement to prevent it from harming your business.

In the last 24 months, 46% of surveyed companies reported experiencing financial crimes like corruption or fraud. This accounts for nearly half the market, which means that the majority of businesses remain unprotected.

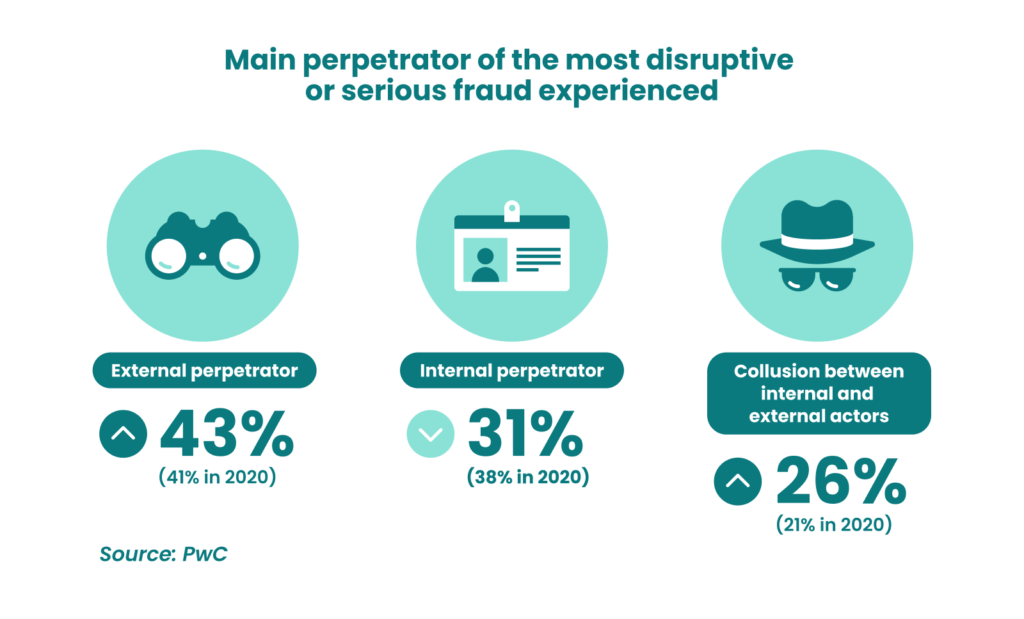

According to 70% of the organizations that were victims of crime reports that the biggest incidents come from 3 places:

External attacks Internal attacks Collision of external and internal sources SourceThe risks are all around - and they are bigger than we can even acknowledge. Two to five percent of the global GDP is being laundered every year, which can go up to $2 trillion. And yet, this is just what we know. Ninety percent of the laundering activities in the world go undetected every year.

These numbers aren’t here to devastate you. They are here to prompt you to take action to prevent fraud to the best of your abilities.

Whatever business you are in or whatever position you have in the distribution chain, you should learn how to mitigate these risks. And in this article, we’ll teach you about the best ways to do this!

Understanding the different forms of financial crime

Before we jump into the tips on how to prevent fin crime, we should discuss the most common forms that you might come across.

Trade-based money laundering

When a criminal uses trade transactions because they want to disguise the movement of cash that isn’t clean, they over-invoice services or falsify invoices. It can also be categorized as invoice fraud.

Pump-and-dump

This form of financial fraud happens when criminals inflate the price of a cryptocurrency or a stock, but only artificially to make it more attractive to buyers. They then sell it off and reap the profits.

Layering

This refers to moving money around through more than one account and many smaller transactions to make them harder to trace.

Many criminals use shell companies based in different countries to make it hard to find the true owner of the money. It’s also a method to hide embezzled money.

Identity theft

Identity theft is everything from misusing someone else’s identification documents to stealing their credit card information. It refers to the usage of another person’s personal information for financial gain.

For example, if you don’t protect your customer’s data, someone might steal their personal details and use them to apply for a loan.

Insurance fraud

When someone makes an insurance claim for an incident by exaggerating it or for something that never happened, that is considered a fraud crime.

For example, an employee can misstate the amount of damage to get more worker's compensation.

Insider trading

Insider trading involves trading in a company’s secrets, securities, stocks, and other information on behalf of employees with third parties.

Tax loss harvesting

Traders, investors, and businesses always try to pay as little task as possible. They often do this by selling underperforming assets to offset capital gains taxes. This is why governments introduced the wash sale rule - to prevent people from taking advantage of the tax code.

Keep in mind that these are just a few of the financial crime incidents that can happen in or to an organization. There are many ways to scam people today, especially with easy access to technology. And we need to talk about avoiding this in your company.

Relate » How to Avoid Day Trading Scams

Tips to prevent financial crime in your organization

Financial crime today is more present, more advanced, and harder to detect. As the Association of Certified Financial Crime Specialists (CFCS) says: “It doesn’t matter what field you work in, it is not the same as it once was.”

Knowing this, here are some tips that can help you protect your business today.

1. Perform KYC checks to verify who you’re doing business with

KYC or Know Your Customer is frequently used in banking. It is actually a legal requirement in the field, demanding that institutions know who they are doing business with to avoid financial crime. Performing these checks sounds pretty straightforward, but it can actually be slow and expensive.

One great tip is to do a pre-KYC check to filter out the junk users instantly, as well as to reduce the costs that come with it. If you gather data early, this can be very useful for risk monitoring.

To simplify and improve the KYC verification and processes, you should use an end-to-end fraud prevention solution.

SEON is partnering with AML and KYC specialists to offer high-quality insights on customers and filter out bad applications for organizations. This will allow you to gather better data for the customer due diligence processes, save on KYC costs, and automate the process for filtering out bad applications.

SourceBanking anti-money laundering or AML is different from KYC verification. It often comes bundled with it to make the work of financial institutions more secure. Generally speaking, the 4 goals of KYC are:

Validate the customer's identity Avoid money laundering Protect the bank’s operations Ensure that customers will receive the financial products and servicesThese days, this isn’t limited to banks only. KYC, and even its electronic version eKYC is used by neobanks, challenger banks, and other financial institutions that move away from the traditional, brick-and-mortar model.

The consequences of failing to implement KYC checks can be severe:

Bigger risks of crime. Criminals that can fool your KYC checks will use this opportunity to create multiple accounts and resell them. Not doing KYC checks can increase your risk of being a victim of financial crime. Heavy fines for non-compliance. These fines amounted to $10.4 billion in 2020 for financial institutions in the world. Today, AML laws applicable to financial institutions exist on a global level. Damage to your reputation. We often see scandals related to financial institutions on the news. If there’s a penalty and a fine, this hardly goes unseen by the news industry and can seriously harm the organization’s reputation.If this goes to the extreme, it can even mean the end of the financial institution. Banks can lose their license if they break the KYC laws repeatedly.

Related » Why Reputation Management Matters For Financial Services

2. Stay compliant with the privacy laws

It sounds obvious, but you’d be surprised by the number of companies that aren’t compliant with the laws that apply to them.

Privacy is paramount in businesses that deal with customer data. In the last couple of years, the regulations and privacy laws have changed tremendously, making sure that businesses protect the information their consumers provide.

SourceTake, for example, the CCPA regulations. Many think that these only apply to organizations doing business in the state of California. However, the California Consumer Protection Act of 2018 changed the rules for who has to comply.

Starting January 1, 2023, the California Privacy Rights Act applies that if you are a for-profit organization that collects the personal data of Californians, you need to comply with the regulations even if your company isn’t based in the state.

Related » The Impact of ASIC Imposed Regulations on the Trade Market

It’s hard to keep track of all laws, especially with changes being enacted regularly. Make sure you don’t do it alone to keep your organization compliant and safe from crime. Osano has created software packages that you can use to:

Gather, track, and document consent Conduct risk assessments Produce privacy notices Respond to access, deletion, and correction requests Manage your third-party data sharing and contracts Source3. Know all the rules and regulations that apply to your organization

Depending on what your organization does, you’d have to adhere to rules and regulations. Make sure you know all about the rules that apply to you. If it’s counter-productive to follow them, find a way to go around them i.e. avoid the rule.

Take, for example, the Pattern Day Trader (PTD) rule. This rule was introduced by the US Congress and is overseen by the Financial Industry Regulatory Authority. According to the rule, a trader who opens more than 4 trades per week in a margin account must have a minimum balance of $25,000 at all times.

Now, this is a high amount and you probably want to avoid the rule without paying hefty fines. To do so, you can:

Stop using leverage in your trading. If you don’t have leverage, you can execute as many trades as you want. Join a prop trading firm. This is a company that will give you capital to use and share the profits with you.Of course, the other option is to remain within the confines of the rule i.e. open less than 4 trades per week.

Ready to make your organization safer?

It is your responsibility to protect your business and the data you use for its operations to the best of your abilities. Hopefully, these tips will help you make your operations and organization safer.